How long could the pain possibly last? Let’s learn more about past economic downturns and speculate on how the current one might look.

Although business cycle ebbs and flows are common and frequently follow patterns that can provide clues about potential future economic downturns, recessions can be extremely painful.

“Recessions come around like the seasons of the year,” says Jonathan Slain, author of “Rock the Recession.” “Although the cause is unknown, we are certain that there will be one.”

Table of Contents

What Is A Recession?

Although it isn’t sufficient on its own, a recession is typically characterized by at least two consecutive quarters of declining GDP (gross domestic product) following a period of growth. The National Bureau of Economic Research (NBER), which is responsible for business cycle dating, defines recessions as “a significant decline in economic activity spread across the economy, lasting more than a few months, normally visible in real GDP, real income, employment, industrial production, and wholesale-retail sales.”

Definition Of A Recession

Let’s start with the fundamentals: what exactly is a recession? It’s a term that’s frequently used to describe any kind of downturn, but there is a fairly clear definition: it typically refers to two or more consecutive quarters of negative GDP growth, which is the total value of everything that the nation produces and is determined by the Bureau of Economic Analysis (BEA).

To count quarters in this situation, we’re not quite there yet. After all, the market didn’t start to decline until March, with March 9 marking the beginning of the initial freefall. However, no one needs to wait to find out how it ends to realize that it will probably be a ugly conclusion.

The National Bureau of Economic Research (NBER) offers a different interpretation of a recession that incorporates a wider range of economic variables. It defines a recession as “a significant decline in economic activity spread across the economy, lasting more than a few months, normally visible in GDP, real income, employment, industrial production, and wholesale-retail sales.” Doesn’t that sound eerily familiar?

And because of this, most experts believe that we have already entered a recession based on these various criteria, rather than waiting for those two quarters of negative GDP growth.

How Do Recessions Start?

Recessions in the past have happened for a variety of reasons, but they typically result from economic imbalances that must ultimately be fixed. For instance, the 2008 recession was brought on by too much mortgage debt, whereas the 2001 recession was brought on by an asset bubble in technology stocks. Another factor that may be to blame is an unexpected shock, such as the COVID-19 pandemic, which was severe enough to hurt business profits and result in job losses.

Consumer spending typically declines in response to rising unemployment, which puts additional strain on business earnings, the economy, and stock prices. These elements may feed a vicious cycle that brings down an economy. Recessions are a natural and necessary way of getting rid of excesses prior to the next economic expansion, despite the fact that they can be difficult to go through.

As Capital Group vice chair Rob Lovelace recently noted, “Without the occasional downturn to keep things in balance, such a long period of growth is impossible. It’s expected and usual. It’s healthy.”

The Typical Recession Lasts How Long?

In a mathematical equation, you add up a lot of numbers and divide them by the total number of numbers. This makes the concept of an average very simple to understand. However, averages frequently fail to provide a complete picture of a situation. What is the typical size of a dog? It all depends on whether or not the dogs are of the same breed. Recessions are the same, and they all differ in their own unique ways.

The average length of a recession since World War II has been reported by the NBER to be approximately 11 months. Of course, we can find an average. But tell that to someone who lived through the Great Recession of 2008, and they’ll say “I wish!” Because every recession is different and has its own distinct features, it can be challenging to predict how long or severe a particular recession will last.

Recessions come in different types, often brought to you by the letters “V” “U,” “W” and “L.” Here are the various ways they pronounce the word relief.

- A V-shaped recession has a nauseating decline and a powerful rebound after it reaches the trough.

- The trough of a U-shaped recession is less distinct. After a while of bouncing along the bottom, it begins to rise again.

- A W recession is also called a “double-dip” recession; it goes down, comes back up, then goes down and back up again—hopefully, this time to stay.

- An L recession is marked by a sharp decline followed by a protracted period of nothingness. In fact, this is most often called a “depression.”

If you guessed that “V” looks most palatable, most would agree. Take a quick fall and come back stronger than ever.

The fact that economists are currently at odds over how the future will pan out demonstrates how, generally speaking, it can be challenging to compare recessions because their causes are typically so diverse.

Examining a few previous recessions serves as an illustration of that.

Examples Of Past Recessions

NBER estimates that since 1854, there have been 33 recessions. It just so happens that the first one it recorded and the most recent one (before the present one) were both 18 months.

The “Panic of 1857,” which lasted from The first recession on the NBER list occurred from June 1857 to December 1858. The Ohio Life Insurance and Trust Company’s failure served as the impetus for the failure of more than 5,000 businesses.

More recent recessions include:

- November 1973 to March 1975 saw a severe oil shortage. The Organization of Petroleum Exporting Countries (OPEC) oil embargo in 1973, which was followed by the removal of the gold standard, wage-price controls, and a quadrupling of oil prices, was blamed for triggering the crisis.

- More than 1,000 savings and loans in the nation failed during the Savings and Loan Crisis, which lasted from July 1990 to March 1991.

- The Internet bubble and 9/11 Attacks (March to November 2001) was a classic “bubble burst” as the economy saw the boom and then bust of the “dot-com” economy, exacerbated by the 9/11 attacks.

- The subprime mortgage crisis, which caused the housing market to collapse and a subsequent bank crisis, was the primary cause of the Great Recession of 2008 (December 2007 to June 2009).

How Long Might The Current Recession Last?

This recession stands out from others because it appeared to stop flowing almost immediately. One might wish for the pain to end in the same manner—quickly—if that were the case. Yet it’s unlikely the world will re-open with a big flip of the switch; in fact, New York Governor Andrew Cuomo has described the process of re-opening businesses as being more like turning a “dial.”

While some activity might pick up once some workplaces reopen in May and beyond, consumers might remain wary until testing is more widely available and a vaccine is available. Federal Reserve Chairman Jerome Powell says he anticipates that “the economic rebound, when it comes, can be robust” once the virus spread is under control and the world returns to work and play. The majority of people, he believes, anticipate that to occur in the second half of the year, though he declined to provide a timeline.

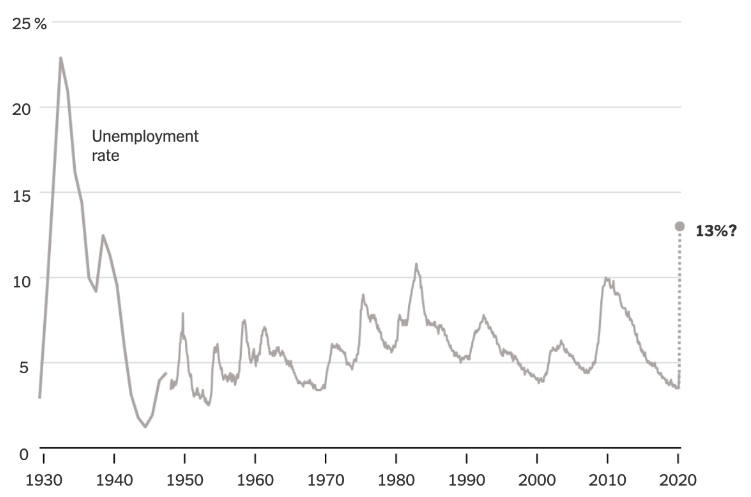

The data, however, is quite depressing. The 22.4 million jobs created since the Great Recession were recently celebrated. By April, that slate had been cleared. As of April 23, 26.45 million Americans had requested unemployment benefits since the start of the pandemic. When compared to the Great Recession, 8.7 million jobs were lost.

Numbers like those are stoking concerns that we may even be entering a depression, which is essentially a severe recession. Usually, a three-year period of severe economic contraction is defined as one in which the GDP has decreased by at least 10%. Other indicators—which we currently have in abundance—include high unemployment and low consumer confidence.

But despite the fact that unemployment is on the rise and the economy is suffering, it’s important to see the bright side: Historically, every stock market downturn has been followed by a strong recovery, and there’s no reason to think that the same will not be true in this case. In fact, keeping a long-term perspective is what makes now a great time to invest.

We can all look to the future and what we can only hope is just a short period of additional turbulence, followed by a high-speed elevator back to the top. While nobody is enjoying this wild recession ride, we can all look to what we can only hope is a brighter future.

What Should You Do With Your Money During A Recession?

Your credit card debt must be paid off. Why? Because most other investments won’t yield an 18% return during a recession, whereas paying off a credit card with an 18% interest rate roughly equates to receiving a return on your investment.

However, as long as rising interest rates aren’t the cause of the recession, bond prices typically increase in value during a downturn.

Recessions: Do They Have A Federal Reserve Cause?

Since maintaining a strong economy is a part of the Fed’s dual mandate, it is officially stated that the Fed never wants to start a recession. The Fed’s dual mandate, which includes keeping inflation low, is regrettably the other aspect. Raising interest rates, which slows the economy, is the primary remedy for rising inflation. Three-month T-bills had a yield of over 15% in 1981 as a result of a Fed interest rate increase that was so extreme. These rates stopped inflation and slowed down the economy, but at the cost of a brief but severe recession.